While geopolitical instability in the Middle East has been a constant for decades, its financial impact is rarely uniform. Historically, as seen during the 1973 Arab Oil Embargo where prices surged 300% in five months, the primary mechanism has been commodity price volatility. Today, with the top three regional exporters generating over $600bn in annual crude revenue, any supply-side disruption triggers an immediate recalibration of global inflation expectations and corporate discount rates. This article analyses the ‘Winners and Losers’ of the current 2026 tension, moving beyond broad macro trends to examine specific impacts on sector-level EBITDA margins and WACC.

Now that the weekend has past we can finally see the impacts of this on the real world. The cost of goods for firms like airlines will increase due to the supply side shocks. Normally, firms would have been able to offset this with hedging or futures trading but in this instance the disruption in global travel will send shockwaves throughout the market. However, many airlines only hedge 40-60% of their fuel therefore if the supply side shock was prolonged for more than a few months the hedges may expire and require new purchases at higher spot rates.

The firms have limited pricing power as they are not able to transfer these increase costs onto the consumer. We can see the impacts of the war on the BASF stock. As at 11 February 2026 the stock had seen almost a year high figure of 51.62 euros however since the escalation the price of the stock has dropped to 47.33 euros as of 2 March 2026.

The Lufthansa stock has also seen a rapid decline moving from 9.43 on the 26th February to 8.57 as of the 2nd March. The impacts have also hit the oil market with Crude oil increasing in price by 7% and Brent increasing in price by around 8%. For airlines fossil fuel costs are the largest variable cost associated with the business thus severely impacting operations. As fuel is the largest variable cost, a 10% increase in Brent Crude often leads to a 20-30% drop in Operating Income because airlines cannot raise ticket prices fast enough to match the pump. Airlines also carry high Fixed Costs. If Net Income drops, their Debt-to-EBITDA ratios worsen, which could lead to credit rating downgrades.

The presumed winners would be the defence companies and the oil companies. Firms like Shell would be able to increase their profit margins as they increase the price of oil due to the supply side shocks. The strait of Hormuz is vital for this. The passage that allows large amount of oil exports to leave the middle east between Iran and Oman. As Iran has closed the strait it would further impact the supply side of oil and relative commodities. The impact of this would be again an increase in the cost of commodities. If the halt within the strait of Hormuz continues it could prevent 15m barrels of oil being transported on a daily basis. As mentioned previously the price of a barrel of oil has already increased by $7 and this would be expected to continue to increase. About 20% of all oil supplies and about 20% of seaborne gas tankers pass through the strait of Hormuz. What could this mean for airlines?

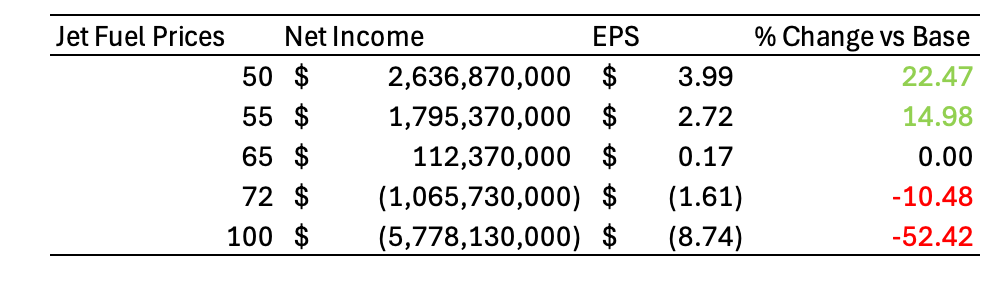

The diagram above shows the sensitivity to jet fuel prices for an American airline. The figures are taken from actual 2025 American Airlines data. The calculations are very rough but do demonstrate the potential impacts of the jet fuel prices on net income and thus earnings per share for American Airlines.

The divergence in performance between Shell and Lufthansa illustrates a broader market recalibration of risk. For airlines, the closure of the Strait of Hormuz impacting 20% of global seaborne gas and oil isn’t just a temporary cost spike; it is a threat to Operating Leverage. If the blockade persists, we expect a ‘sector-wide’ downward revision of FY26 EPS estimates as higher fuel costs intersect with potentially cooling consumer demand.

Conversely, for Defence and Upstream Energy, this volatility acts as a valuation floor. The market is currently pricing in a ‘Geopolitical Risk Premium’ that favours companies with ‘Hard Asset’ exposure. The primary question for analysts now is not if costs will rise, but how long these supply-side shocks will stay ‘sticky’ before they trigger a broader contraction in global discretionary spending.

Note: Figures were accurate as of 1 March 1.30pm